A team to guide you

Our team of advisors guide you through various retirement scenarios, quantify your goals and plan for life’s uncertainties before crafting a retirement plan that aligns with the future you envision.

If you are approaching retirement, you're getting ready to make some very important financial decisions. One of the most critical will be when you decide to claim Social Security.

Before discussing how potential increases to your Social Security benefit work, let’s understand the best way to determine the monthly benefit you’re entitled to given your earnings record. The simplest way to do this is by logging into your account at ssa.gov and downloading a recent annual statement from the Social Security Administration.

On the top right corner on the first page of your statement, you’ll notice a monthly benefit amount (known as your Primary Insurance Amount). This is the monthly benefit you currently have available to you at your Full Retirement Age (FRA). NOTE: depending on your earnings record and how far away from retirement you are, this number might change substantially.

As many of you know, you have the option to claim this monthly benefit before your FRA as early as age 62 (resulting in a LOWER monthly payment), or you can delay your benefit as late as age 70 (resulting in a HIGHER monthly payment).

The purpose of this article is to help you understand how the benefit increases work if you decide to delay past your FRA.

What Determines My Social Security Payment Amount?

We now know delaying between your Full Retirement Age (FRA) and age 70 will increase your Social Security payments, but by how much?

There are two important factors that go into your increased benefit when deferring – your delayed retirement credits (DRC) and any annual cost-of-living adjustment (COLA) increases.

Let’s quickly define these two items:

Delayed Retirement Credits (DRC): This is an increase in the monthly benefit amount due to a retiree deferring collecting his/her benefit past their Full Retirement Age. Think of it as a “thank you” from the government for not taking money out of the Social Security system yet!

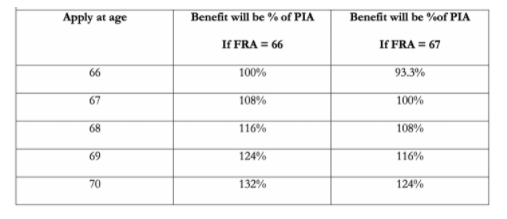

Here is a summary of how your FRA increases with age:

Summary of how your FRA increases with age

For example: Mary has a Full Retirement Age of 66 but has decided to wait until age 68 to begin collecting her benefit. She will receive an additional 8% increase in her benefit for delaying from 66 to 67, and another 8% for delaying from age 67 to 68 for a total benefit increase of 16%!

Cost-of-Living Adjustment (COLA): This is the annual increase the government gives your Social Security benefit amount based on inflation, so that retiree's benefits can “keep up” with life getting more expensive over time. Federal benefit rates increase when the cost of living rises, as measured by the Department of Labor’s Consumer Price Index (CPI-W).

For example: if the inflation index used for benchmarking Social Security benefits rises by 4% in a given year, the government will subsequently raise your monthly benefit by roughly 4% for the following year.

You may have heard COLA discussed in the context of those already claiming benefits, but one question we’ve heard from clients is “will I be forfeiting the COLA increase by delaying my benefits?” The answer: No. If you defer benefits past your FRA, you are entitled to both the DRC and COLA.

Combining our two previous examples, if Mary delayed from age 66 to 67 and the COLA adjustment for Social Security benefits over the same year was 4%, her combined benefit increase would be 12% (an 8% delayed credit for deferring one year along with the 4% inflation adjustment).

For a full breakdown of how Social Security is calculated, check out our previous blog

There are several additional planning considerations that you will want to review before deciding your Social Security filing election, such as your need for income. If you’re looking for a Social Security analysis, click here to contact our team of advisors.

The Burney Company is an SEC-registered investment adviser. Burney Wealth Management is a division of the Burney Company. Registration with the SEC or any state securities authority does not imply that Burney Company or any of its principals or employees possesses a particular level of skill or training in the investment advisory business or any other business. Burney Company does not provide legal, tax, or accounting advice, but offers it through third parties. Before making any financial decisions, clients should consult their legal and/or tax advisors.