A team to guide you

Our team of advisors guide you through various retirement scenarios, quantify your goals and plan for life’s uncertainties before crafting a retirement plan that aligns with the future you envision.

At the halfway point in the year (June/July), it is important to focus on mid-year tax considerations. While it probably feels like you just filed your 2022 return, setting aside some dedicated time for mid-year tax planning can help you save on your 2023 tax bill and eliminate surprises when it comes time to file next year.

Wealth Advisors Brenna Surette, CFP® and Bijal Patel, CFP® explain the importance of mid-year tax planning and steps you can take.

Why is it important to be proactive with tax planning? It first might help to understand the differences between tax preparation and tax planning.

Tax preparation is what we are most accustomed to. It involves plugging numbers into a tax filing software around the start of tax time each year and then waiting anxiously as the system crunches the numbers to tell us if we owe or will be getting a refund.

Tax planning, on the other hand, is an ongoing process that involves monitoring your tax situation throughout the year and making adjustments where needed. This will help you stay on track and can ultimately lead to tax savings and limited tax time surprises. There are two ways to approach tax planning; you can do it yourself by researching ideas and spending time on the IRS website, or you can work alongside a qualified financial or tax advisor.

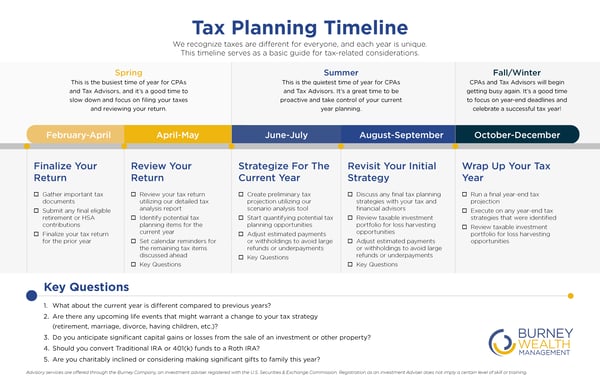

Click on the tax planning timeline graphic above to download a free 1-page PDF.

Here are a few tax planning considerations we like to implement with our clients:

Tax Planning Step #1: Review Your return

Reflecting on and learning from your previous tax return is a great place to get started. A detailed analysis should reveal any missed tax savings opportunities or areas for improvement.

You (and/or your trusted tax or financial advisor) should make sure you understand the following:

i) Your Marginal Tax Bracket: In the US we have a progressive tax system, which means different levels of income are taxed at different rates. Your marginal tax rate is the tax rate you would pay if you earned an additional $1 of income. Which bracket did you fall into for the year? Do you anticipate a change in your income for 2023? A change in income could mean a change in your marginal tax bracket which might mean any of the following:

- You may qualify for certain deductions or credits you weren’t eligible for before

- You may want to consider certain opportunities that might make sense, such as a Roth conversion

- You may need to change your withholdings from your paycheck or estimated quarterly payments

ii) Your Tax Rate on Investment Income: What tax rate did you pay on your qualified dividends and capital gains? Is your portfolio as tax efficient as it could be?

- Many investors aren’t aware that there are several tax brackets for capital gains. This is important to know when it comes to making decisions on how to invest inside of your portfolio and when to take action with your investments throughout the year.

- Your marginal tax rate might also come in handy again when it comes to evaluating how tax efficient your investments are: should you consider tax-free municipal bonds? Are you holding the right types of investments in the appropriate accounts based on tax treatment?

iii) Deductions: Did you itemize or pay the standard deduction?

- This plays a role in important decisions such as allocating charitable giving and medical expenses. Understanding how close you are to itemizing versus taking the standard deduction might lead you to take certain tax saving action this year versus next year. For example, someone who is about to retire next year (and subsequently see their earned income/tax rate drop) might decide to “accelerate” several years of planned charitable giving into the year before retirement to take advantage of itemizing charitable deductions in a higher tax year.

iv) Any expected changes: Your tax analysis should serve as a reference point throughout the year and should be revisited as your situation changes.

Need help? Click here to schedule a complimentary tax analysis!

Tax Planning Step #2: Strategize for the Current year

Another important checkpoint will be to build an income tax projection for the current and future tax years. The goal of a tax projection is to estimate your income tax liability based on potential future life changes or investment activity. For example, do you anticipate a big raise? Are you transitioning into retirement soon? Did you need to realize a large capital gain this year from the sale of an investment or a business? Changes in income are an important “tipping point” for knowing when taking certain actions might improve your future tax situation.

Here are some common strategies and tips related to tax projections we like to discuss with our clients:

i) Roth Conversions: Roth conversions involve transferring funds (aka converting) from a pre-tax retirement account into a Roth retirement account. When you do this, you’ll need to pay federal and state taxes on the amount converted and be mindful of certain restrictions. Once inside of the Roth account the funds will grow tax-deferred and be eligible for tax free withdrawals in the future. This can be a significant tool to build wealth for the future.

Why might this make sense? Every situation is unique and there are several reasons to consider a conversion, but generally If you expect your tax rate to be higher in the future it makes sense to consider taking action.

IMPORTANT TIP: A common scenario we see is individuals that reach age 73 and must start taking their Required Minimum Distribution alongside pension, social security, and other income sources. The combination of all this income can quickly bump them into a higher tax bracket than planned, which can put a strain on their financial resources. Utilizing Roth conversions before age 73 to get in front of this may help reduce your future tax obligations and allow your financial assets to last longer.

ii) Managing Required Minimum Distributions (RMD): You will want to make sure you take your distribution before the end of this year to avoid a hefty 50% penalty.

As we mentioned earlier, RMDs may push you into a higher tax bracket than expected. We covered Roth conversions as a helpful strategy to reduce this potential future tax obligation, but another strategy you may want to take advantage of is a Qualified Charitable Distribution (QCD). A QCD is a direct transfer of funds from your IRA to a qualified charity. This distribution will be excluded from your taxable income, making it a great way to lower your tax burden while supporting an important cause at the same time.

Tax strategies like those mentioned above should be considered in the context of a comprehensive financial plan. Talk with your tax, legal, or financial advisor to determine if any of the above makes sense for you.

Taxes don’t need to feel like a daunting chore. Working with a financial advisor can allow you to be proactive and help you identify potential savings opportunities. Contact us to get started.

The Burney Company is an SEC-registered investment adviser. Burney Wealth Management is a division of the Burney Company. Registration with the SEC or any state securities authority does not imply that Burney Company or any of its principals or employees possesses a particular level of skill or training in the investment advisory business or any other business. Burney Company does not provide legal, tax, or accounting advice, but offers it through third parties. Before making any financial decisions, clients should consult their legal and/or tax advisors.